India invented the Unified Payments Interface (UPI) through the National Payments Corporation of India (NPCI).

Launched in 2016, it revolutionized digital payments by allowing millions of users to conduct real-time, mobile-first, cashless transactions. Its ease of use, security, and 24-hour availability have made it a pillar of India’s digital economy.

In this article, we’ll look at how UPI came to be, who created it, and why this distinctively Indian idea has become a global standard for fast payments.

Which Country Invented The UPI ID? – Origin Of UPI

The Unified Payments Interface (UPI), also known as a UPI ID, was developed in India by the National Payments Corporation of India (NPCI) to enable fast, secure, and seamless digital payments.

Established in 2008 by India’s financial authorities, NPCI aimed to build a uniform and efficient payment ecosystem. UPI allows users to transfer money through a virtual payment address without sharing bank details.

Officially launched on April 11, 2016, UPI has become central to real-time mobile banking. By August 2, 2025, it had recorded an estimated 700 million transactions.

History of UPI – Why The UPI System Was Created

India’s UPI revolutionized digital payments by enabling secure, real-time transfers across multiple bank accounts on one mobile platform, strengthening India’s digital economy globally.

Let us look at the evolution of UPI through the years:

2008 – NPCI Conceptualized

The idea of a central payment infrastructure was first proposed in 2008 to provide a streamlined, standardized digital payments system for Indian banks. This laid the framework for the UPI system, which would eventually affect payments.

2010 – NPCI Established

In 2010, the National Payments Corporation of India (NPCI) was established with the aim of managing retail payment systems and promoting digital transactions across the nation. It became the basis of India’s unified payment vision.

2016 – UPI Launched

UPI was introduced in April 2016, and the notion of virtual payment addresses (UPI IDs) is utilized to facilitate fast bank-to-bank transfers via mobile applications. It made mobile payments far more convenient and secure.

2018 – Mobile Wallet Integration

With the introduction of UPI in major mobile wallets and apps, it gained popularity and was used by millions. This connection enabled users to purchase, recharge, and transfer money from within familiar apps, thereby increasing adoption.

2025 – Cross-Border Pilot

Starting in 2025, UPI began working with banks across the United Arab Emirates and Singapore.

The introduction of this experiment resulted in near-real-time international payments, solidifying India’s position as a world leader in digital payments.

UPI vs Other Global Payment Systems

India’s UPI is a leading real-time payment system offering fast, secure, mobile-first transactions, surpassing PayPal, Faster Payments, and SEPA Instant with 24/7, QR, and cross-border capabilities.

The situation in 2025 is as follows:

| Feature | UPI (India) | PayPal (Global/USA) | Faster Payments (UK) | SEPA Instant (Euro‑zone) |

|---|---|---|---|---|

| Real‑time / Instant Transfers | Yes, domestic payments settle in seconds. Cross-border via UPI–PayNow (Singapore) also near real-time. | Partial, PayPal instant transfers depend on bank/card rails; standard withdrawals take 1–3 business days. | Yes, near-instant domestic transfers, 24/7. | Yes, euro transfers within SEPA zone in seconds. |

| Bank-to-Bank Direct Settlement | Yes, direct account-to-account via UPI. | Partial, wallet-based; bank transfers depend on instant withdrawal options. | Yes, FPS moves money directly between UK bank accounts. | Yes, SEPA Instant moves funds directly between euro-zone accounts. |

| 24/7 / Year-round Availability | Yes, 24/7, including holidays. | Partial, depends on user’s bank and region. | Yes, always available. | Yes, 24/7/365 within SEPA zone. |

| QR Code Payments | Yes, widely used across India for merchants and peer-to-peer payments. | Yes, supported via PayPal QR codes in select countries for merchant payments. | Limited, some banks/apps support QR codes, but not natively part of the FPS rail. | Limited, QR-based payments depend on specific bank apps or PSPs, not standard SEPA rail. |

| Cross-Border / International Payments | Limited / Growing, UPI–PayNow (India–Singapore), and pilots expanding. | Yes, global transfers are supported, but speed varies by currency, country, and bank. | No, domestic only. | Limited to SEPA zone (euro transfers). |

Global Impact of India’s UPI Innovation

India’s Unified Payments Interface (UPI) has transformed and greatly impacted digital payments in the global financial ecosystem.

Its real-time, mobile-first architecture and simplicity have helped to establish a global standard for cashless, inclusive payment solutions.

Here is how India’s UPI Innovation has an impact on the global level:

- Cross-border adoption:

UPI has started working with banks in Singapore and the UAE, enabling near-real-time international transfers. - Influence on FinTech innovation:

With its simplicity and speed, UPI has transformed digital payment methods globally, prompting governments to develop mobile-first, instant-settlement systems similar to India’s. - Financial inclusion:

UPI has become an emerging standard, connecting millions of people to formal banking channels by enabling peer-to-peer and merchant payments via mobile phones. This is a lesson to other developing nations. - Global recognition and partnerships:

The international interest in UPI has prompted central banks and payment companies to cooperate with other countries, leading to experimental programs that highlight India’s leadership in real-time digital payment infrastructure.

Related Reads:

Conclusion: India Is The Inventor Of UPI ID

NPCI developed the UPI ID in 2016. This innovation revolutionized digital banking. It allows fast, mobile-first, and secure money transfers.

Users can send money from one bank to another without needing traditional account details.

The UPI is executing over a million transactions daily and is also expanding into cross-border payments, underscoring India’s real-time digital finance capabilities.

This growth showcases India’s leadership in real-time digital finance and demonstrates how UPI has made digital payments easier, faster, and more accessible for millions of users.

FAQs

The NPCI’s excellent architecture, real-time settlement systems, cloud-based infrastructure, and seamless interface with banks and fintech apps helped India achieve this scale.

Yes. UPI IDs will enable cross-border payments through agreements with banks in Singapore and the UAE by 2025.

UPI is notable for its capacity to process real-time bank transfers, QR code payments, and cross-border transactions. However, PayPal is reliant on wallet rails; Faster Payments is available domestically, and SEPA Instant is restricted to the eurozone.

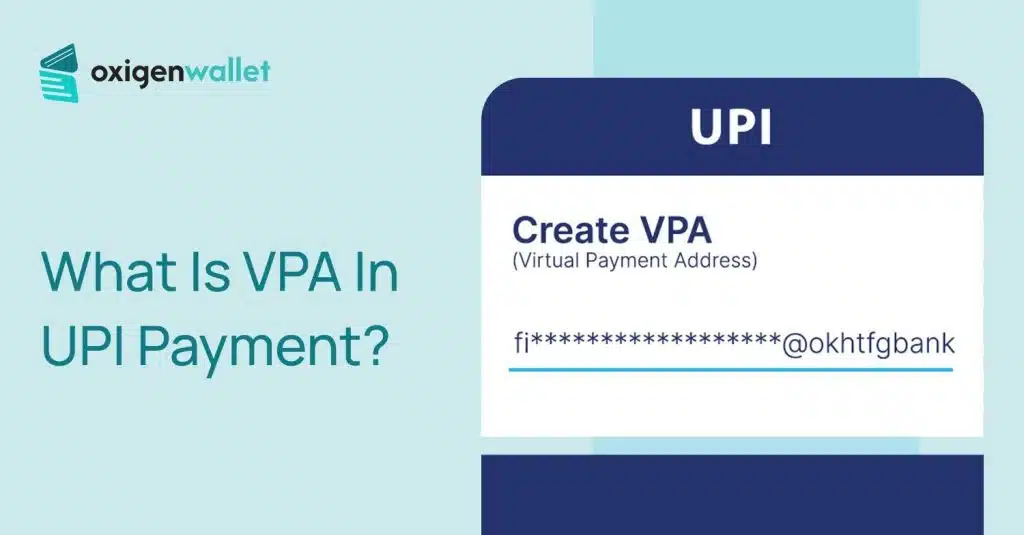

Yes. A UPI ID serves as a Virtual Payment Address (VPA), which means users do not reveal sensitive bank account or IFSC information.